Disruption 2020: Office Fundamentals Weaken

The U.S. office market showed a sharp decline in the second quarter as the impact of the COVID-19 pandemic began to reveal itself fully. Net absorption fell into negative territory for the first time in 10 years, while vacancy posted its largest quarterly increase in the same period. Construction levels remain elevated, although the timing of some projects is being reassessed. Asking rents are holding steady for the time being. Sales volume fell significantly, to its lowest second quarter total in 10 years, while, with a limited amount of transactional evidence, capitalization (cap) rates held firm.

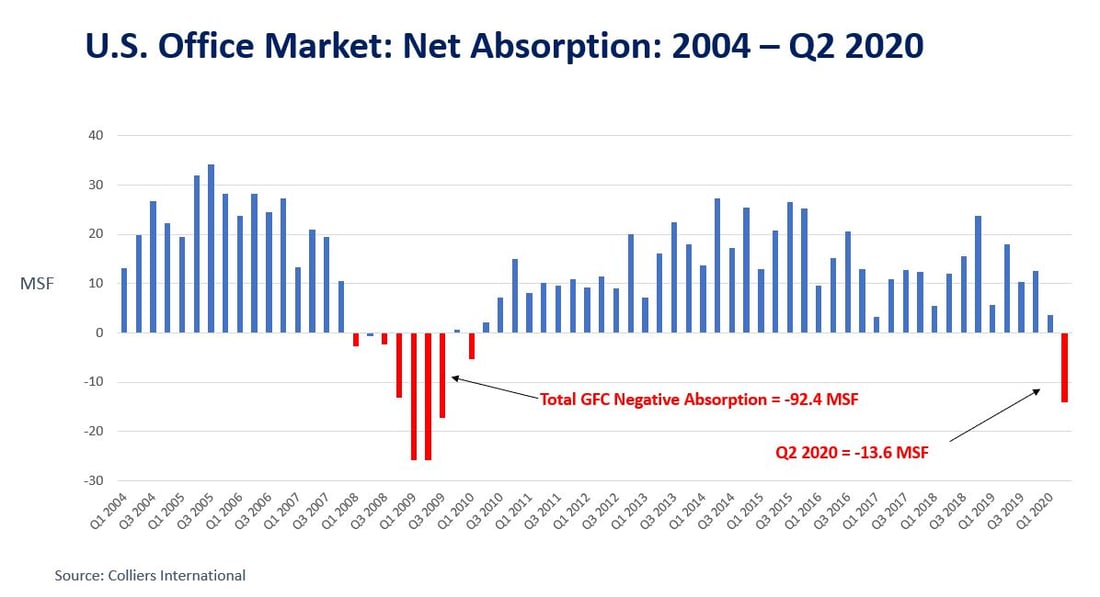

Here are some of the headline numbers from Q2 2020:

- The U.S. office vacancy rate rose by 40 basis points to 11.9%, the highest quarterly increase in vacancy since Q1 2010.

|

- U.S. office absorption fell into negative territory for the first time since Q1 2010 at -13.6 million SF. Office absorption declined by 86% year-over-year.

|

- Two-thirds of office markets recorded negative absorption in the second quarter, led by a combined negative 6.1 million SF in New York, Boston, and the Bay Area.

|

- Rents are, for the most part, holding firm, but declines look to be in the offing. Any growth is increasingly limited and found in markets such as Austin, Nashville, Philadelphia, and South Florida.

|

- The amount of office space under construction in the U.S. rose marginally to 156.7 million SF. Construction volume in the previous cycle peaked at 125.2 million SF in Q2 2008.

|

- Sales volume totaled $11 billion, down from $29.4 billion in the first quarter. The year-over-year sales total is down by 71.4%.

|

With businesses taking a very tentative approach to returning to the workplace, the impact on office sector metrics will take some time to fully emerge. While there was a marked downturn in Q2 2020, the true test will be the second half of the year. It may take several quarters and multiple phases of reopening before firms can fully assess their space needs.

What are the prospects for office demand? The depth and length of the coronavirus recession will be a key determinant, as will future patterns and levels of occupancy. Many urban centers are showing very limited physical occupancy today. To what extent could firms downsize their footprints, particularly in downtown locations, and will a portion of jobs shift to being permanently home-based? These questions cannot be answered yet.

With decision making largely on hold, transactional evidence is limited at best. Look for rents to find a new ceiling once a clearer picture on corporate occupancy emerges. Expect a similar pattern of price discovery in the sales market.

Should there be a major flow of sublease space onto the market, it should be competitively priced, creating the potential for direct rents to drop as landlords seek to compete. We are already beginning to see sublease inventory increase markedly in Boston and San Francisco. The initial decline in direct rates should be more prevalent in older commodity space. Where asking rates do hold up, this will likely be due to increased incentives that thereby lower net effective rents.

|

GO SOCIAL

Share with your network

|

|

|

|

AUTHOR(S):

|