Disruption 2020: Hotels Capital Markets Trends

The COVID-19 pandemic has brought unprecedented disruption to the U.S. lodging sector. Travel restrictions, quarantines and global air travel pullback have rocked hotel fundamentals. How that disruption may affect both recovery and hotel investors is the focus of today’s post.

COVID-19 Pandemic Disruption

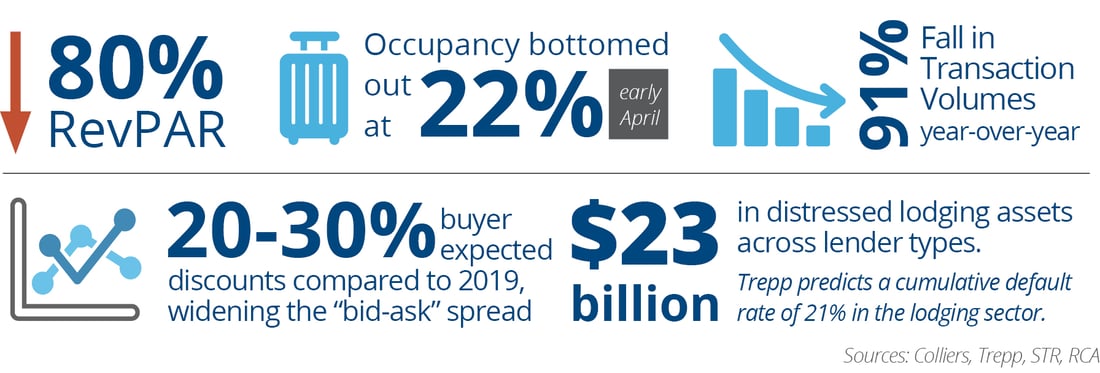

- RevPAR fell 80%. Occupancies bottomed out at 22% in early April; rebounding to 48.1% in late July per STR.

- Owners/investors have tried to preserve liquidity, including temporary and outright closures, furloughs/layoffs, PPP loan applications, drawdowns on FFE reserve, negotiating forbearance on mortgages and deferring CAPEX and brand-mandated improvements.

- Short-term rentals — Airbnb and the like — are recovering more quickly than hotels, due to demand for “staycations” and a need for local short-term housing. Short-term rentals will remain a formidable lodging player, and their 10% U.S. market share is expected to grow.

|

Capital Markets Insight

- Hotel transaction volumes fell 91% year-over-year, per Real Capital Analytics, totaling just $643 million in the second quarter.

- Values are dropping — RCA’s CPPI declined by 5.4% in June YTD. With so few transactions, pricing discovery is difficult, exacerbated by buyers expecting 20%–30% discounts to 2019, widening the traditional “bid-ask” spread.

- Much equity capital is targeting hotel acquisitions; debt acquisition financing is limited.

|

Emerging Distress

- RCA is tracking $23 billion in distressed lodging assets across lender types. Due to less clarity about the status of non-CMBS loans, this figure could rise. The second round of forbearance negotiations is ongoing.

- Trepp predicts a cumulative default rate of 21% in the lodging sector, far more than that for other asset types. The current LTV of these loans is 41.5, with a DSCR of 2.14. Trepp forecasts a peak-to-trough price change of negative 47.9%.

- Balance sheet lenders are more accommodating to borrower work-out requests than are debt fund and CMBS lenders. Note sales are just beginning.

|

Recovery

- Economy, Midscale limited-service, and extended-stay hotels are performing relatively better than Upper Upscale and Luxury (UU/L). Economy rooms drove 41% of demand in May 2020 but 25% in May 2019, while UU/L decreased from 21% to 8% year-over-year.

- Secondary, tertiary and drive-to leisure markets are expected to outperform big cities.

- Some expected permanent closures are a welcome macro trend in some markets, notably New York, with excess supply.

- STR and other firms project that U.S. hotel performance might not return to 2019 levels until 2023.

|

The market turbulence represents opportunity for astute investors for the foreseeable future. The recovery in the hotel market is a matter of if, only when. We believe in a strategy of “flight-to-quality” acquisition of newer, premium-branded Midscale, Upscale and extended-stay hotels in markets with diverse demand drivers. Despite the current price discovery challenges, the quality-focused intuitive and aggressive buyer with access to capital will thrive.

New development remains attractive, although caution is advised. There are 215,000 rooms under construction, more than the previous peak in December 2007. New hotels with the latest technology will command a market premium. Inevitably, distressed hotels will be offered as viable hotel acquisitions, but buyers must be sure that investment targets have upside in branding, CAPEX and management. |

|

GO SOCIAL

Share with your network

|

|

|

|

AUTHOR(S):

|